Decision trees are one of the major data structures in machine learning. Their

inner workings rely on heuristics which, while satisfying to our intuitions,

give remarkably good results in practice (notably when they are aggregated into

"random forests"). Their tree structure also makes them readable by human

beings, contrary to other "black box" approaches such as neural networks.

In this tutorial, we will see how decision trees work and provide a few

theoretical justifications along the way. We will also (briefly) talk about

their extension to random forests. To get started, you should already be

familiar with the general setting of supervised learning.

Training of a decision tree

A decision tree models a hierarchy of tests on the values of its input, which

are called attributes or features. At the end of these tests, the predictor

outputs a numerical value or chooses a label in a pre-defined set of options.

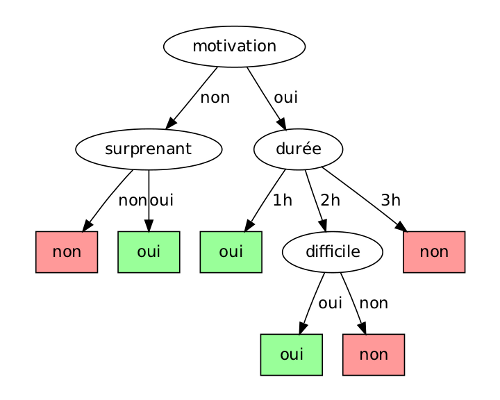

The former is called regression, the latter classification. For instance,

the following tree could be used to decide if a French student finds a lecture

interesting or not, i.e. classification in the binary set {oui, non}

(French booleans ;p), based on the boolean attributes {motivation,

surprenant, difficile} and a discrete attribute durée ∈ {1 h, 2

h, 3 h}. We could also have made the last one a continuous attribute, but we'll

come back to that.

The input to our decision is called an instance and consists of values for

each attribute. It is usually denoted by (x,y) where y is

the attribute the tree should learn to predict and x=(x1,…,xm) are the m other attributes. A decision tree is learned on a

collection of instances T={(x,y)} called the training set.

Example of training set for the decision tree above

| date |

motivation |

durée (h) |

difficile |

surprenant |

température (K) |

|---|

| 11/03 |

oui |

1 |

non |

oui |

271 |

| 14/04 |

oui |

4 |

oui |

oui |

293 |

| 03/01 |

non |

3 |

oui |

non |

297 |

| 25/12 |

oui |

2 |

oui |

non |

291 |

| ... |

... |

... |

... |

... |

... |

Given our observations T={(x,y)}, we now want to build a

decision tree that predicts y given new instances x. As of

today (2011) there are essentially two families of algorithms to do this:

Quinlan trees and CART trees. Both follow a divide-and-conquer

strategy that we can sum up, for discrete attributes, by the following

pseudocode:

1: DecisionTree(T: training set):

2: if "stop condition":

3: return leaf(T)

4: choose the "best" attribute i between 1 and m

5: for each value v of i:

6: T[v] = {(x, y) from T such that x_i = v}

7: t[v] = DecisionTree(T[v])

8: return node(i, {v: t[v]})

In what follows, we use uppercase T for training sets and lowercase

t for trees. A tree is either a leaf leaf(T), where we save a

subset T of the original training set, or a node node(i, {v:

t[v]}) that tests attribute i and has a child tree tv for

each potential value v of the attribute. The two statements with

quotation marks correspond to heuristics specific to each algorithm:

- Stop condition:

- The condition used to decide when it is time to produce an answer rather

than grow the tree to better fit the data. For instance, the condition

∣T∣=1 will produce detailed trees with excellent score on the

training set (for each instance (x,y)∈T the tree will

predict exactly y given x) but quite deep and not likely

to generalize well outside of this set due to overfitting.

- Best attribute:

- The goal of this heuristic is to evaluate locally what attribute yields the

"most information" on (or is the "most correlated" to) the result to

predict. We will see examples of such criteria below.

When learning a continuous attribute xi∈R, we adapt the

above pseudocode by selecting a split value v corresponding to a test

xi≤v. We will denote by node(i, v, t[≤], t[>]) the

corresponding node constructor. In the particular case where all attributes are

continuous, the resulting decision tree is a binary tree.

Regression

Let us consider first the case of regression, that is, when the value to

predict is a real number. Once our tree is built, regressing a new instance

x amounts to traversing a branch as follows:

1: Regress(x, t)

2: if t is a leaf(Tf):

3: return the average of y's in Tf

4: else if t is a node(i, v, t_left, t_right):

5: if x[i] <= v:

6: return Regress(x, t_left)

7: else (x[i] > v):

8: return Regress(x, t_right)

9: else (t is a node(i, {v -> t[v]})):

10: return Regress(x, t[x[i]])

This exploration ends up in a leaf f built on a training set

Tf, which we denoted in pseudocode as leaf(Tf). Let us define

Yf:={y∣∃(x,y)∈Tf}. The value predicted at the

end of the regression process is the average y of

Yf. The more the distribution of y∈Yf is concentrated

around y, the better the prediction will be. Equivalently,

the higher the dispersion of these values, the worse the prediction. CART trees

thus use the variance σ2 of Yf to measure

this dispersion and evaluate the "quality" of the leaf f.

Choosing a split attribute

CART also uses this variance criterion to choose the best split attribute at

line 4 of our DecisionTree(T) constructor. A given attribute i

yields a partition T=∪viTvi of the training set

T, where each subset Tvi has its own variance

V(Tvi). Variance after selecting i as split

attribute is then, for an instance (x,y) drawn uniformly at random

from T:

Vi=vi∑∣T∣∣Tvi∣V(Tvi)The attribute i∗ that minimizes this value is (heuristically)

considered as the best attribute. We will see in the next section how this

choice of minimizing variance is not only heuristic: it is also intrinsically

linked to minimizing a mean squared error.

Why minimize variance?

One of the main assumptions in machine learning is that instances (x,y) are drawn independently from the

same unknown probability distribution P. We can therefore see our

(x,y)∈T as realizations of i.i.d.

random variables X and Y (the two of them possibly

correlated). Similarly, leaf values y∈Yf are i.i.d. realizations

of the random variable Yf obtained by conditioning Y upon the

events {Xi≤ or >v} tested along the branch from

the root of our decision tree to the leaf f. With this in mind, we can

interpret y as an estimator for E(Yf). Its

mean squared error is then:

E[(Yf−y)2]=E[(Yf−E(Yf)+E(Yf)−y)2]=(y−E(Yf))2+E[(Yf−E(Yf))2]In this calculation, y and E(Yf) are

constants. The second term in the final sum is exactly the variance

σ2 of Yf, which CART trees estimate via

σ2. Minimizing σ for a leaf

f thus aims at minimizing this second term, but also the first one!

Since y is an arithmetic average

y=∣Yf∣1y∈Yf∑y=k1i=1∑kYf[i]of realizations of Yf (the random variable, not the set of

values—sorry for the overlapping notations), we have

ET(y)=E(Yf) and

VT(y)=σ2/n. Here the index T

means that expectations are taken over all possible training sets with fixed

size ∣T∣=n, with the size of the leaf set also fixed ∣Yf∣=k. Consequently, Markov's inequality yields:

P[(y−E(Yf))2>x]<kxσ2,which shows handwavingly how minimizing the variance σ will also

concentrate the distribution of y around

E(Yf), and thus reduce the first term in the mean squared

error of our estimator.

Classification

The logic for classification is similar to regression:

1: Classify(x, t)

2: if t is a leaf(Tf):

3: return the majority class in Tf

4: else if t is a node(i, v, t_left, t_right):

5: if x[i] <= v:

6: return Classify(x, t_left)

7: else (x[i] > v):

8: return Classify(x, t_right)

9: else (t is a node(i, {v -> t[v]})):

10: return Classify(x, t[x[i]])

If a majority of instances in Tf belong to the same class c∈{1,…,C}, then c is the best prediction we can make, and the

fraction ∣{(x,y)∈Tf∣y=c}∣/∣Tf∣ of instances in

Tf that belong to class c is an indicator of the "sureness" of

our prediction. When this ratio is roughly the same for all classes, predicting

the most frequent class in Tf still sounds reasonable, yet keeping in

mind that the quality of the prediction is low.

Measuring leaf homogeneity

These observations highlight how in classification a decision tree is all the

better when (the instances in) its leaves are homogeneous. We can then measure

the heterogeneity of a leaf the same way we measured variance for regression.

Let p1,…,pC denote the relative frequencies of classes

c∈{1,…,C} in Tf, and let c∗=argmaxipi denote the most frequent class. There are three main leaf heterogeneity

measures in the literature:

- Error rate:

- e(Tf):=1−pc∗, the classification error rate of our

algorithm over the training set.

- Gini criterion:

- e(Tf):=∑cpc(1−pc), which corresponds to the

classification error rate over the training set of a randomized algorithm

that would return class c with probability pc (rather than

deterministically returning c∗). This measure is used in CART

trees.

- Entropy:

- e(Tf):=−∑cpclogpc, which estimates the entropy of the class c from an

instance (x,c) drawn uniformly at random from Tf. This

measure is used in ID3 and C4.5 trees.

Choosing a split attribute

The leaf heterogeneity measure is also used to select the split attribute: if

an attribute i partitions T into T=∪viTvi, then every sub-tree Tvi has its own heterogeneity

e(Tvi). The error we expect from our prediction after branching to

the next sub-tree, for an instance drawn uniformly at random from T, is

accordingly:

ei=vi∑∣T∣∣Tvi∣e(Tvi)The attribute i∗=argminiei that minimizes this error is

(heuristically) considered as the best attribute, to be used at line 4 of our

DecisionTree(T) constructor.

Extensions

Decision trees as we described them have a number of limitations:

- The overall optimization problem is NP-complete for several optimality

criteria, which is why we

turned to heuristics.

- The learning procedure is static: trees are not designed to learn

incrementally from new instances that would continuously extend the training

set.

- They are sensitive to noise and have a tendency to overfit, that is, to

learn relationships between both data and noise present in the training set.

There are solutions to these problems that work directly on trees, notably

pruning (more details here and here).

In practice, it is often more convenient to go for one of the techniques that

follow, bagging and random forests, to alleviate overfitting while keeping the

implementation simple.

Bagging

The word bagging is an acronym for "bootstrap aggregating". It is a meta-algorithm that combines two techniques, guess which:

- Bootstrapping:

- a bootstrap of set T is another set obtained by drawing ∣T∣

times elements from T uniformly at random and putting them back.

Bootstrapping from a training set T yields a new set T′

that has on average 1−e−1≈63% unique instances from

T, when T is a big set.

- Aggregating:

- suppose we produce a sequence of bootstraps T1′,…,Tm′, and

we use each bootstrap Ti′ to train a predictor ti (for us

it will be a decision tree, although the technique could apply to any

family of predictors). Given an instance (x,y), we regress each

tree to obtain a set of predictions y1,…,ym, and

aggregate them into an arithmetic average y=∑iyi/m.

Bagging improves decision trees on several points: it smoothens out their

instability (where small perturbations in the training set can yield a

completely different tree due to the selection of a different early splitting

attribute), and makes predictions that are less sensitive to overfitting. The

price to pay is a loss in readability: bagged predictions are not the product

of a "reasoning", as was the case with a singular decision tree, rather a

consensus over several "reasonings" that potentially look at radically

different sets of attributes.

As of 2011, our theoretical understanding of bagging is still fairly limited: a

few arguments help us understand its impact and suggest conditions in which

they improve predictions, but we don't have a clear model in which we can

express and measure this impact.

Random forests

Proposed in 2002 by Leo Breiman and Adele Cutler, random forests

modify the DecisionTree(T) constructor to build trees that are better

suited to bagging. There are two main changes:

- Attribute sampling:

- Line 4 of our algorithm, rather than choosing i in the set of

available attributes A={1,…,m}, we draw a subset

A′⊂A of size ∣A′∣=m′≤m uniformly at random

(for regression, the authors suggest m′≈m/3) and choose our

heuristically best attribute i∗ in A′. The goal of this

step is to reduce the correlation between the several trees we train from

the same training set, e.g. avoiding that they all choose the same split

attribute at the root if one attribute turns out to seem consistenly better

than the others, allowing for "independent thought" in a fraction of the

trees that choose to ignore it at first. Intuitively, correlation means

consensus, and too strong of a consensus reaps off the benefits of bagging.

- Stop condition:

- Trees are grown as deep as possible, i.e., our stop condition happens as

late as possible (for instance ∣Tf∣<10 or ∣Yf∣=1)

within the limits of our computation power. Thus, our predictors try to

learn as much as possible from their data, their individual overfitting and

sensitivity to noise in the training set being compensated for later by

bagging.

For further details on random forests, see the manuscript by Breiman and

Cutler, or the The Elements of Statistical Learning: Data Mining, Inference,

and Prediction by Hastie

et al.

To go further

You can find the algorithms described above implemented in Python with SQLite

in the PyDTL library, which is

open source and distributed under the LGPLv3 license. It draws from both CART

and C4.5 trees and is geared toward growing random forests. Decision trees are

also implemented in other software such as milk (Python), Orange and Weka (Java).

Here comes the end of our introduction to decision tree learning. There are

likely many points to improve in it: feel free to write me if you have any

question or suggestion. For a deeper study of these techniques, and of

supervised learning in general, I highly recommend The Elements of Statistical

Learning: Data Mining, Inference, and Prediction by Hastie et al.

This tutorial is a translation of Une introduction aux arbres de décision, a note I wrote in 2011 after my internship at

INRIA with Marc Lelarge. Warm thanks to

Marc for supporting this work, for our discussions, and the cool topics we

worked on :-)

Discussion

Feel free to post a comment by e-mail using the form below. Your e-mail address will not be disclosed.